This is scary…

This is scary…

Posted in Climate Change

Tagged 5th assessment, above 1.5°C, agricultural productivity, anthropogenic greenhouse gas, atmospheric concentrations, biological carbon stores, carbon dioxide, carbon emission, climate change, climate change resilience, climate models, climate resilient pathways, climate system, climate warming, COP24, decarbonized economy, emissions reductions, geological data sets, global warming, greenhouse gas emissions, IPCC, IPCC 2018 report, IPCC assessment, methane hydrates, ocean carbon sinks, Paris Agreement, permafrost thaw, population growth, pre-industrial temperatures, sea level, soil erosion, synthesis reports, temperature increase, tipping elements, Trump climate change, UN climate talks

As we enter a week where further market turmoil is likely against a background of further tensions between the US and China over the Huawei arrest, the climax of the Brexit debacle, and the yellow vest protests in France. All these issues can and will be resolved eventually but they pale in comparison to the political inaction over the latest climate change reports.

The US government, in the form of the United States Global Change Research Program (USGCRP), in a report in November concluded that “the evidence of human-caused climate change is overwhelming and continues to strengthen, that the impacts of climate change are intensifying across the country, and that climate-related threats to Americans’ physical, social, and economic well-being are rising” and warned that “these impacts are projected to intensify—but how much they intensify will depend on actions taken to reduce global greenhouse gas emissions and to adapt to the risks from climate change now and in the coming decades”. Of course, the Orange One again demonstrated his supreme myopic attitude with the dismissal “I don’t believe it”.

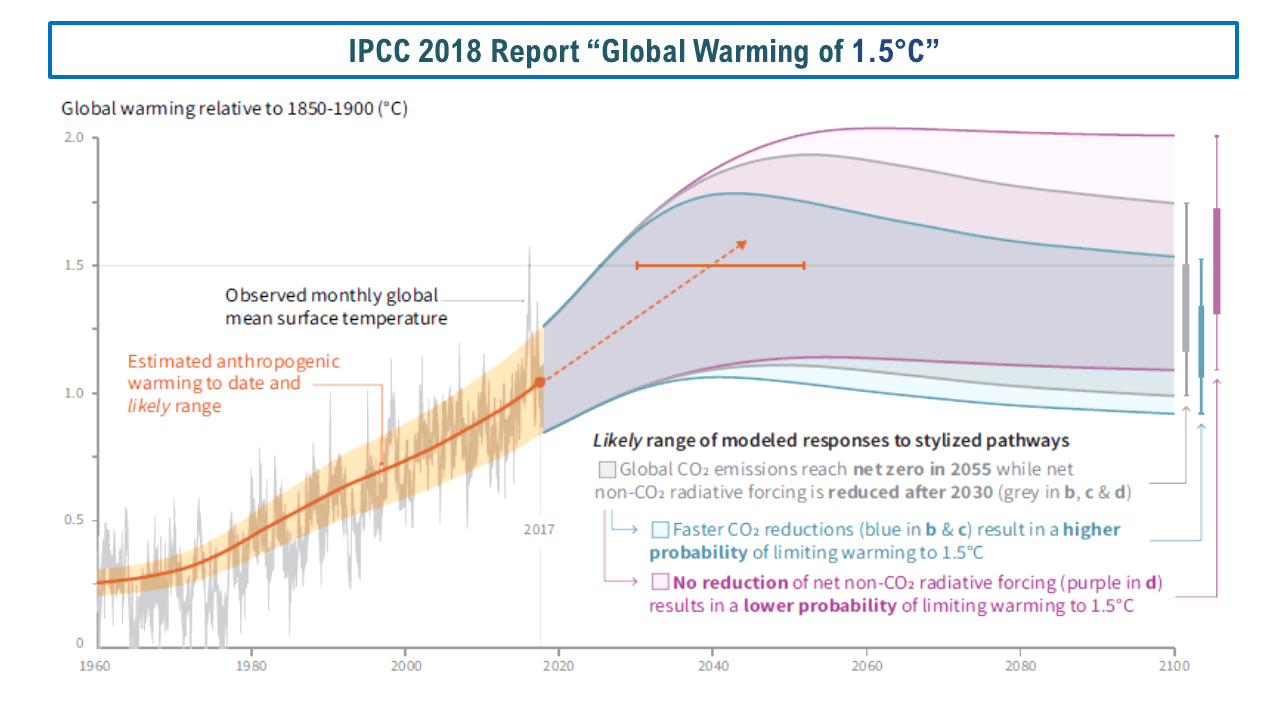

We now have the black comedy of oil producing states such as the US, Russia and Saudi Arabia arguing over whether to “welcome” or just “note” the latest IPCC report this week at the UN climate talks, known as COP24. The IPCC report on the impacts of a temperature rise of 1.5°C was launched last October and is a sobering read. The IPCC again states with a high level of confidence that “human activities are estimated to have caused approximately 1.0°C of global warming above pre-industrial levels, with a likely range of 0.8°C to 1.2°C” and that “global warming is likely to reach 1.5°C between 2030 and 2052 if it continues to increase at the current rate”.

click to enlarge

In order to avoid warming above 1.5°C, the world needs “global net anthropogenic CO2 emissions decline by about 45% from 2010 levels by 2030 (40–60% interquartile range), reaching net zero around 2050 (2045–2055 interquartile range)”. For limiting global warming to below 2°C, emissions need to “decline by about 25% by 2030 in most pathways (10–30% interquartile range) and reach net zero around 2070 (2065–2080 interquartile range)”.

Let’s face it, given the current political leadership across the globe, such declines are just fantasy. And I find that really depressing. The plea of David Attenborough at COP24 last week for leaders in the world to lead looks set to fall on deaf ears. Attenborough worryingly stated that “the continuation of our civilisations and the natural world upon which we depend, is in your hands (i.e. our leaders)”.

We’re pretty much toast then….

Posted in Climate Change

Tagged 5th assessment, above 1.5°C, agricultural productivity, anthropogenic drivers, anthropogenic greenhouse gas, atmospheric concentrations, biological carbon stores, carbon dioxide, carbon emission, climate change, climate change resilience, climate models, climate resilient pathways, climate system, climate warming, COP24, decarbonized economy, emissions reductions, geological data sets, global warming, greenhouse gas emissions, IPCC, IPCC 2018 report, methane, methane hydrates, National Academy of Sciences, nitrous oxide, ocean carbon sinks, Paris Agreement, permafrost thaw, PNAS, population growth, pre-industrial temperatures, sea level, soil erosion, synthesis reports, tipping elements, Trump climate change, UN climate talks, uninhabitable, USGCRP

In an opinion piece in the FT in 2008, Alan Greenspan stated that any risk model is “an abstraction from the full detail of the real world”. He talked about never being able to anticipate discontinuities in financial markets, unknown unknowns if you like. It is therefore depressing to see articles talk about the “VaR shock” that resulted in the Swissie from the decision of the Swiss National Bank (SNB) to lift the cap on its FX rate on the 15th of January (examples here from the Economist and here in the FTAlphaVille). If traders and banks are parameterising their models from periods of unrepresentative low volatility or from periods when artificial central bank caps are in place, then I worry that they are not even adequately considering known unknowns, let alone unknown unknowns. Have we learned nothing?

Of course, anybody with a brain knows (that excludes traders and bankers then!) of the weaknesses in the value-at-risk measure so beloved in modern risk management (see Nassim Taleb and Barry Schachter quotes from the mid 1990s on Quotes page). I tend to agree with David Einhorn when, in 2008, he compared the metric as being like “an airbag that works all the time, except when you have a car accident“. A piece in the New York Times by Joe Nocera from 2009 is worth a read to remind oneself of the sad topic.

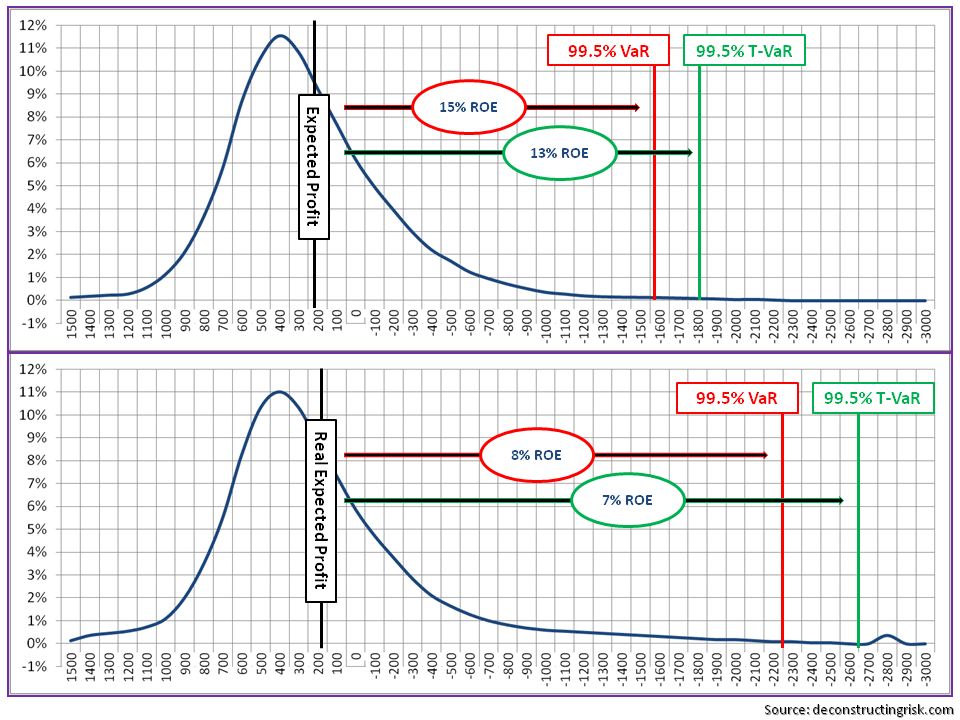

This brings me to the insurance sector. European insurance regulation is moving rapidly towards risk based capital with VaR and T-VaR at its heart. Solvency II calibrates capital at 99.5% VaR whilst the Swiss Solvency Test is at 99% T-VaR (which is approximately equal to 99.5%VaR). The specialty insurance and reinsurance sector is currently going through a frenzy of deals due to pricing and over-capitalisation pressures. The recently announced Partner/AXIS deal follows hot on the heels of XL/Catlin and RenRe/Platinum merger announcements. Indeed, it’s beginning to look like the closing hours of a swinger’s party with a grab for the bowl of keys! Despite the trend being unattractive to investors, it highlights the need to take out capacity and overhead expenses for the sector.

I have posted previously on the impact of reduced pricing on risk profiles, shifting and fattening distributions. The graphic below is the result of an exercise in trying to reflect where I think the market is going for some businesses in the market today. Taking previously published distributions (as per this post), I estimated a “base” profile (I prefer them with profits and losses left to right) of a phantom specialty re/insurer. To illustrate the impact of the current market conditions, I then fattened the tail to account for the dilution of terms and conditions (effectively reducing risk adjusted premia further without having a visible impact on profits in a low loss environment). I also added risks outside of the 99.5%VaR/99%T-VaR regulatory levels whilst increasing the profit profile to reflect an increase in risk appetite to reflect pressures to maintain target profits. This resulted in a decrease in expected profit of approx. 20% and an increase in the 99.5%VaR and 99.5%T-VaR of 45% and 50% respectively. The impact on ROEs (being expected profit divided by capital at 99.5%VaR or T-VaR) shows that a headline 15% can quickly deteriorate to a 7-8% due to loosening of T&Cs and the addition of some tail risk.

click to enlarge

For what it is worth, T-VaR (despite its shortfalls) is my preferred metric over VaR given its relative superior measurement of tail risk and the 99.5%T-VaR is where I would prefer to analyse firms to take account of accumulating downside risks.

The above exercise reflects where I suspect the market is headed through 2015 and into 2016 (more risky profiles, lower operating ROEs). As Solvency II will come in from 2016, introducing the deeply flawed VaR metric at this stage in the market may prove to be inappropriate timing, especially if too much reliance is placed upon VaR models by investors and regulators. The “full detail of the real world” today and in the future is where the focus of such stakeholders should be, with much less emphasis on what the models, calibrated on what came before, say.

Posted in Insurance Market, Insurance Models

Tagged 1 in 10000 return period, 99% T-VaR, 99.5% VaR, adverse selection, Alan Greenspan, Barry Schachter, climate models, David Einhorn, deeply flawed VaR metric, dilution of terms and conditions, discontinuities in financial markets, economic capital models, economic modelling, European insurance regulation, exchange rates, fat tails, financial engineering, financial innovation, financial models, FTAlphaVille, game theory, imperfect art of modelling, insurance capital models, insurance pricing pressure, internal capital models, internal models, Joe Nocera, loss exceedance probability distribution, modern risk management, Nassim Taleb, New York Times, probability models, probability of default, probability of occurrence, reducing risk adjusted premiums, Return on equity, return period, risk based capital, risk model, solvency ii, Solvency II calibration, Solvency II standard formula, specialty insurance sector, Swiss National Bank, Swiss Solvency Test, Swissie, tail value at risk, Tails of VaR, the Economist, unknown unknowns, unrepresentative low volatility, value at risk, VaR and T-VaR, VaR shock

So, after the (im)piety of the Christmas break, its time to reflect on 2014 and look to the new year. As is always the case, the world we live in is faced with many issues and challenges. How will China’s economy perform in 2015? What about Putin and Russia? How strong may the dollar get? Two other issues which are currently on traders’ minds as the year closes are oil and Greece.

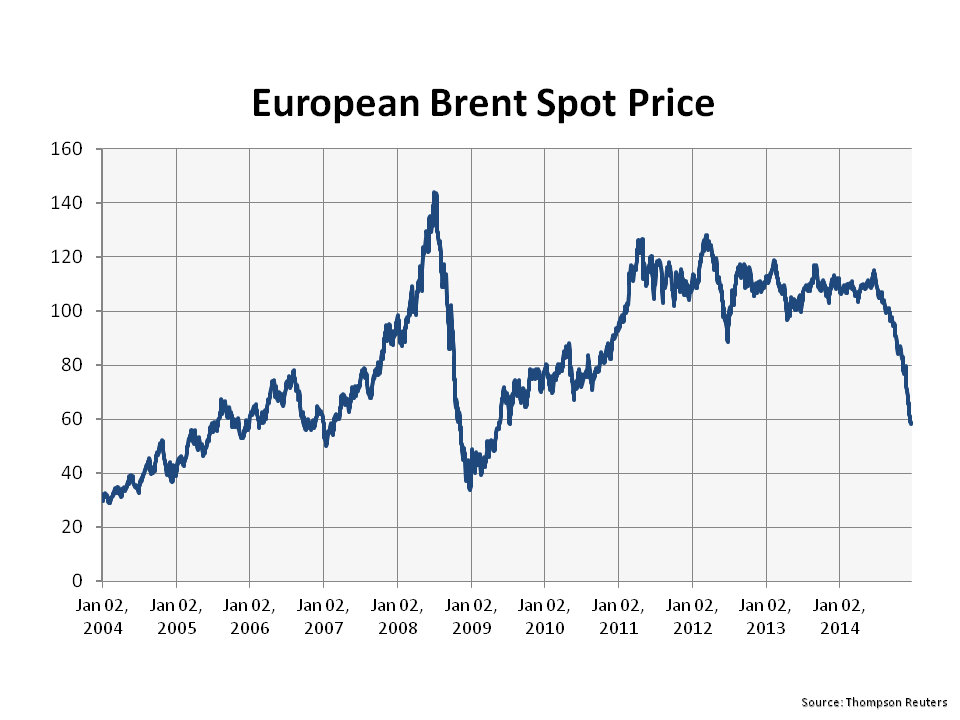

The drop in the price of oil, driven by supply/demand imbalances and geo-political factors in the Middle East, was generally unforeseen and astonishing swift, as the graph of European Brent below shows.

click to enlarge

Over the short term, the drop will be generally beneficial to the global economy, acting like a tax cut. At a political level, the reduction may even put manners on oil dependent states such as Iran and Russia. Over the medium to long term however, it’s irrational for a finite resource to be priced at such levels, even with the increased supply generated by new technologies like fracking (the longer term environmental impacts of which remain untested). The impact of a low oil price over the medium term would also have negative environmental impacts upon the need to address our carbon based economies as highlighted in 2014 by the excellent IPCC reports. I posted on such topics with a post on climate models in March, a post on risk and uncertainty in the IPCC findings in April, and another post on the IPCC synthesis reports in November.

The prospect of another round of structural stresses on the Euro has arisen by the calling of an election in late January in Greece and the possible success of the anti-austerity Syriza party. Although a Greek exit from the Euro seems unlikely in 2015, pressure is likely to be exerted for relief on their unsustainable debt load through write offs. Although banking union has been a positive development for Europe in 2014, a post in May on an article from Oxford Professor Kevin O’Rourke outlining the ultimate need to mutualise European commitments by way of a federal Europe to ensure the long term survival of the Euro. Recent commentary, including this article in the Economist, on the politics behind enacting any meaningful French economic reforms highlights how far Europe has to go. I still doubt that the German public can be convinced to back-stop the commitments of others across Europe, despite the competitive advantage that the relatively weak Euro bestows on Germany’s exporting prowess.

Perpetually, or so it seems, commentators debate the possible movements in interest rates over the coming 12 months, particularly in the US. A post in September on the findings of a fascinating report, called “Deleveraging, What Deleveraging?”, showed the high level of overall debt in the US and the rapid increase in the Chinese debt load. Although European debt levels were shown to have stabilised over the past 5 years, the impact of an aggressive round of quantitative easing in Europe on already high debt levels is another factor limiting action by the ECB. The impact of a move towards the normalisation of interest rates in the US on its economy and on the global economy remains one of the great uncertainties of our time. In 2015, we may just begin to see how the next chapter will play out.

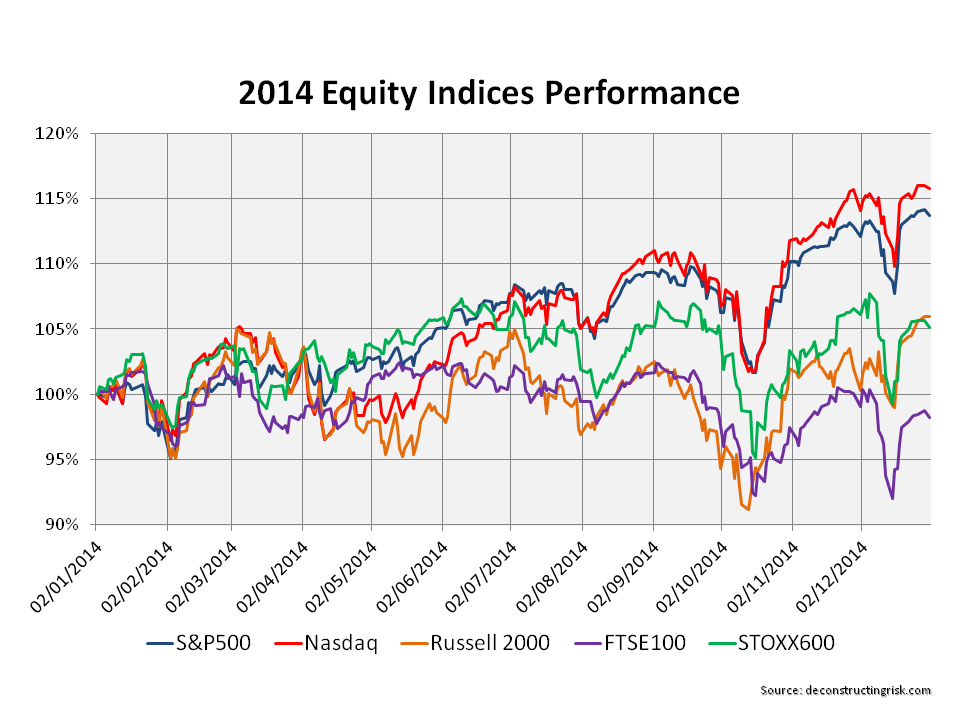

Low interest rates have long been cited as a factor behind the rise in stock market valuations and any increase in interest rates remains a significant risk to equity markets. As the graph below attests, 2014 has been a solid if unspectacular year for nearly all equity indices (with the exception of the FTSE100), albeit with a few wobbles along the way, as highlighted in this October post.

click to enlarge

The debate on market valuations has been an ever-present theme of many of my posts throughout 2014. In a March post, I continued to highlight the differing views on the widely used cyclically adjusted PE (CAPE) metric. Another post in May highlighted Martin Wolf’s concerns on governments promoting cheap risk premia over an extended period as a rational long term policy. Another post in June, called Reluctant Bulls, on valuations summarized Buttonwood’s assertion that many in the market were reluctant bulls in the absence of attractive yields in other asset classes. More recently a post in September and a post in December further details the opposing views of such commentators as Jim Paulsen, Jeremy Siegel, Andrew Lapthorne, Albert Edwards, John Hussman, Philosophical Economics, and Buttonwood. The debate continues and will likely be another feature of my posts in 2015.

By way of a quick update, CAPE or the snappily named P/E10 ratio as used by Doug Short in a recent article on his excellent website shows the current S&P500 at a premium of 30% to 40% above the historical average. In his latest newsletter, John Hussman commented as follows:

“What repeatedly distinguishes bubbles from the crashes is the pairing of severely overvalued, overbought, overbullish conditions with a subtle but measurable deterioration in market internals or credit spreads that conveys a shift from risk-seeking to risk-aversion.”

Hussman points to a recent widening in spreads, as illustrated by a graph from the St Louis Fed’s FRED below, as a possible shift towards risk aversion.

click to enlarge

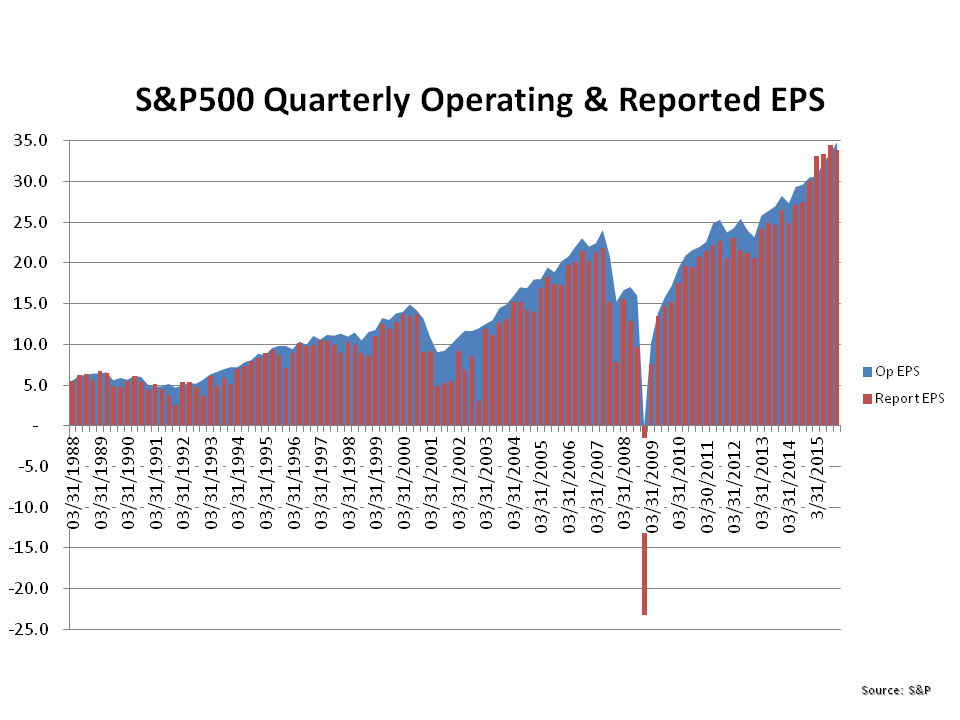

The bull arguments are that valuations are not particularly stressed given the rise in earnings driven by changes to the mix of the S&P500 towards more profitable and internationally diverse firms. Critics counter that EPS growth is being flattered by subdued real wage inflation and being engineered by an explosion in share buybacks to the detriment of long term investments. The growth in quarterly S&P500 EPS, as illustrated below, shows the astonishing growth in recent years (and includes increasingly strong quarterly predicted EPS growth for 2015).

click to enlarge

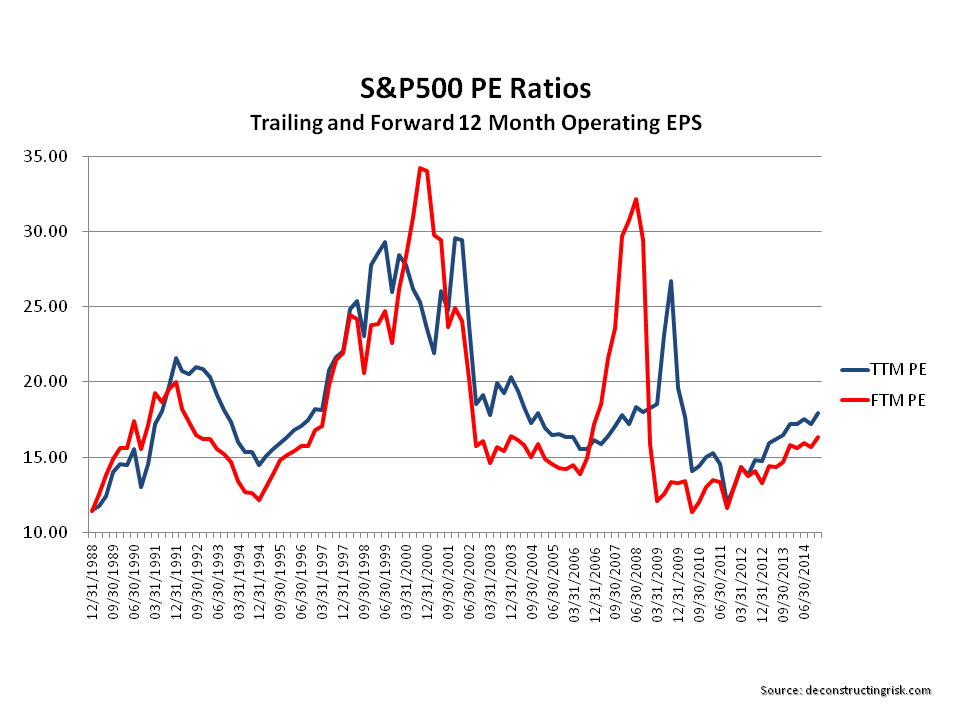

A recent market briefing from Yardeni research gives a breakdown of projected forward PEs for each of the S&P500 sectors. Its shows the S&P500 index at a relatively undemanding 16.6 currently. In the graph below, I looked at the recent PE ratios using the trailing twelve month and forward 12 month operating EPS (with my own amended projections for 2015). It also shows the current market at a relatively undemanding level around 16, assuming operating EPS growth of approx 10% for 2015 over 2014.

click to enlarge

The focus for 2015 is therefore, as with previous years, on the sustainability of earnings growth. As a March post highlighted, there are concerns on whether the high level of US corporate profits can be maintained. Multiples are high and expectations on interest rates could make investors reconsider the current multiples. That said, I do not see across the board irrational valuations. Indeed, at a micro level, valuations in some sectors seem very rational to me as do those for a few select firms.

The state of the insurance sector made up the most frequent number of my posts throughout 2014. Starting in January with a post summarizing the pricing declines highlighted in the January 2014 renewal broker reports (the 2015 broker reports are due in the next few days). Posts in March and April and November (here, here and here) detailed the on-going pricing pressures throughout the year. Other insurance sector related posts focussed on valuation multiples (here in June and here in December) and sector ROEs (here in January, here in February and here in May). Individual insurance stocks that were the subject of posts included AIG (here in March and here in September) and Lancashire (here in February and here in August). In response to pressures on operating margins, M&A activity picking up steam in late 2014 with the Renaissance/Platinum and XL/Catlin deals the latest examples. When seasoned executives in the industry are prepared to throw in the towel and cash out you know market conditions are bad. 2015 looks to be a fascinating year for this over-capitalised sector.

Another sector that is undergoing an increase in M&A activity is the telecom sector, as a recent post on Europe in November highlighted. Level3 was one of my biggest winners in 2014, up 50%, after another important merger with TW Telecom. I remain very positive on this former basket case given its operational leverage and its excellent management with a strong focus on cash generation & debt reduction (I posted on TWTC in February and on the merger in June and July). Posts on COLT in January and November were less positive on its prospects.

Another sector that caught my attention in 2014, which is undergoing its own disruption, is the European betting and online gambling sector. I posted on that sector in January, March, August and November. I also posted on the fascinating case of Betfair in July. This sector looks like one that will further delight (for the interested observer rather than the investor!) in 2015.

Other various topics that were the subject of posts included the online education sector in February, Apple in May, a dental stock in August, and Trinity Biotech in August and October. Despite the poor timing of the August TRIB call, my view is that the original investment case remains intact and I will update my thoughts on the topic in 2015 with a view to possibly building that position once the selling by a major shareholder subsides and more positive news on their Troponin trials is forthcoming. Finally, I ended the year having a quick look at Chinese internet stocks and concluded that a further look at Google was warranted instead.

So that’s about it for 2014. There was a few other random posts on items as diverse as a mega-tsunami to correlations (here and here)!

I would like to thank everybody who have taken the time to read my ramblings. I did find it increasingly difficult to devote quality time to posting as 2014 progressed and unfortunately 2015 is looking to be similarly busy. Hopefully 2015 will provide more rich topics that force me to find the time!

A very happy and health 2015 to all those who have visited this blog in 2014.

Posted in General

Tagged Albert Edwards, andrew lapthorne, anti-austerity Syriza party, banking union, Buttonwood, CAPE, carbon based economies, China economy, Chinese debt, climate models, cyclically adjusted PE, debt write offs, Deleveraging What Deleveraging, Doug Short, environmental impact, equity indices, European Brent, European debt levels, forward PE, fracking, French economic reforms, geo-political factors, Greece, insurance sector, IPCC reports, IPCC synthesis report, irrational valuations, Jeremy Siegel, Jim Paulsen, John Hussman, M&A activity, Martin Wolf, Middle East, normalisation of interest rates, online education sector, online gambling sector, Oxford Professor Kevin O’Rourke, P/E10 ratio, Philosophical Economics, Putin Russia, Reluctant Bulls, Risk & Uncertainty, risk aversion, risk premia, sector ROEs, structural stresses Euro, subdued real wage inflation, sustainability of earnings growth, telecom sector, unsustainable debt load, valuation multiples

The release of the synthesis reports by the IPCC – in summary, short and long form – earlier this month has helped to keep the climate change debate alive. I have posted (here, here, and here) on the IPCC’s 5th assessment previously. The IPCC should be applauded for trying to present their findings in different formats targeted at different audiences. Statements such as the following cannot be clearer:

“Anthropogenic greenhouse gas (GHG) emissions have increased since the pre-industrial era, driven largely by economic and population growth, and are now higher than ever. This has led to atmospheric concentrations of carbon dioxide, methane and nitrous oxide that are unprecedented in at least the last 800,000 years. Their effects, together with those of other anthropogenic drivers, have been detected throughout the climate system and are extremely likely to have been the dominant cause of the observed warming since the mid-20th century.”

The reports also try to outline a framework to manage the risk, as per the statement below.

“Adaptation and mitigation are complementary strategies for reducing and managing the risks of climate change. Substantial emissions reductions over the next few decades can reduce climate risks in the 21st century and beyond, increase prospects for effective adaptation, reduce the costs and challenges of mitigation in the longer term, and contribute to climate-resilient pathways for sustainable development.”

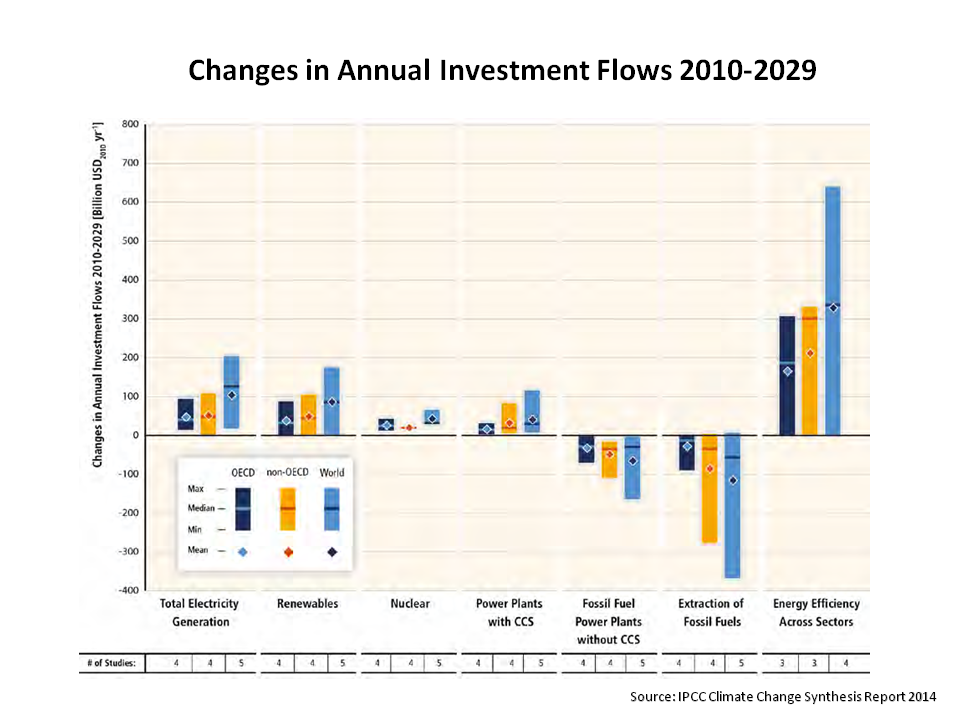

The IPCC estimate the costs of adaptation and mitigation of keeping climate warming below the critical 2oC inflection level at a loss of global consumption of 1%-4% in 2030 or 3%-11% in 2100. Whilst acknowledging the uncertainty in their estimates, the IPCC also provide some estimates of the investment changes needed for each of the main GHG emitting sectors involved, as the graph reproduced below shows.

click to enlarge

The real question is whether this IPCC report will be any more successful that previous reports at instigating real action. For example, is the agreement reached today by China and the US for real or just a nice photo opportunity for Presidents Obama and Xi?

In today’s FT Martin Wolf has a rousing piece on the subject where he summaries the laissez-faire forces justifying inertia on climate change action as using the costs argument and the (freely acknowledged) uncertainties behind the science. Wolf argues that “the ethical response is that we are the beneficiaries of the efforts of our ancestors to leave a better world than the one they inherited” but concludes that such an obligation is unlikely to overcome the inertia prevalent today.

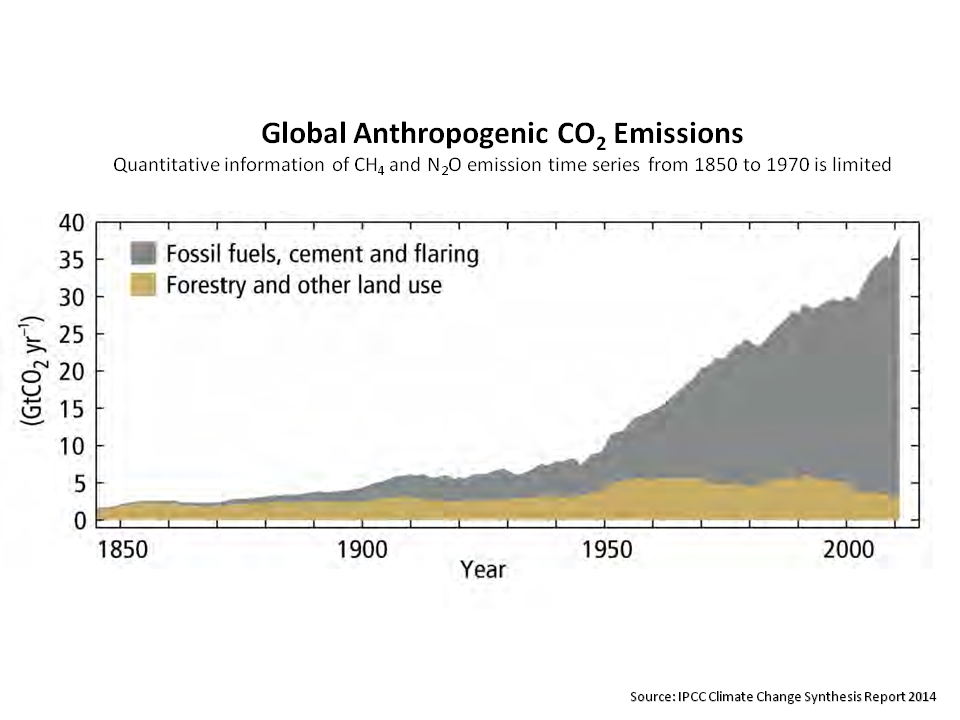

I, maybe naively, hope for better. As Wolf points out, the costs estimated in the reports, although daunting, are less than that experienced in the developed world from the financial crisis. The costs don’t take into account any economic benefits that a low carbon economy may result in. Notwithstanding this, the scale of the task in changing the trajectory of the global economy is illustrated by one of graphs from the report, as reproduced below.

click to enlarge

Although the insurance sector has a minimal impact on the debate, it is interesting to see that the UK’s Prudential Regulatory Authority (PRA) recently issued a survey to the sector asking for responses on what the regulatory approach should be to climate change.

Many industry players, such as Lloyds’ of London, have been pro-active in stimulating debate on climate change. In May, Lloyds issued a report entitled “Catastrophic Modelling and Climate Change” with contributions from industry. In the piece from Paul Wilson of RMS in the Lloyds report, they concluded that “the influence of trends in sea surface temperatures (from climate change) are shown to be a small contributor to frequency adjustments as represented in RMS medium-term forecast” but that “the impact of changes in sea-level are shown to be more significant, with changes in Superstorm Sandy’s modelled surge losses due to sea-level rise at the Battery over the past 50-years equating to approximately a 30% increase in the ground-up surge losses from Sandy’s in New York.“ In relation to US thunderstorms, another piece in the Lloyds report from Ionna Dima and Shane Latchman of AIR, concludes that “an increase in severe thunderstorm losses cannot readily be attributed to climate change. Certainly no individual season, such as was seen in 2011, can be blamed on climate change.“

The uncertainties associated with the estimates in the IPCC reports are well documented (I have posted on this before here and here). The Lighthill Risk Network also has a nice report on climate model uncertainty which concludes that “understanding how climate models work, are developed, and projection uncertainty should also improve climate change resilience for society.” The report highlights the need for expanding geological data sets beyond short durations of decades and centuries which we currently base many of our climate models on.

However, as Wolf says in his FT article, we must not confuse the uncertainty of outcomes with the certainty of no outcomes. On the day that man has put a robot on a comet, let’s hope the IPCC latest assessment results in an evolution of the debate and real action on the complex issue of climate change.

Follow-on comment: Oh dear the outcome of the Philae lander may not be a good omen!!!

Posted in Climate Change, Insurance Models

Tagged 5th assessment, AIR, anthropogenic drivers, anthropogenic greenhouse gas, atmospheric concentrations, carbon dioxide, Catastrophic Modelling and Climate Change, climate change, climate change resilience, climate models, climate resilient pathways, climate system, climate warming, emissions reductions, geological data sets, IPCC, Lighthill Risk Network, Lloyds of London, methane, modelled surge losses, nitrous oxide, Paul Wilson, PRA, Prudential Regulatory Authority, RMS, RMS medium-term forecast, sea level, Shane Latchman, Superstorm Sandy, synthesis reports, US thunderstorms

![]() This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.

This blog represents my personal views and is not reflective of the views or opinions held by any company or employer I work for currently or have worked for in the past. The views expressed herein are based solely upon publicly available data. No views expressed herein should be taken as an endorsement to take any particular course of action in the markets. The basis of this blog is that different views should be expressed and readers make up their own minds on the what they believe and act accordingly.